Trading in a car you haven’t fully paid off can sound tricky—but it’s a common situation and entirely possible if you approach it the right way. Whether your needs have changed, you want to lower your monthly payment, or you’re simply ready for an upgrade, this guide will walk you through exactly how to trade in a financed vehicle, even with a loan balance remaining.

Here’s a step-by-step breakdown of how to do it smartly and avoid costly mistakes.

Step 1: Determine Your Loan Payoff Amount

Before you start shopping for your next car, contact your lender and ask for the payoff amount. This is the total balance remaining on your loan, including interest and any fees needed to close the account early.

Make sure to get a “10-day payoff quote” if you’re planning to trade in soon—this accounts for any interest accruing in the coming days.

Step 2: Find Out Your Car’s Trade-In Value

Next, research the market value of your current car. You can do this by checking:

Kelley Blue Book (KBB)

Edmunds

Carvana / Vroom / CarMax trade-in offers

Dealership appraisal

This gives you a sense of what dealers or third-party buyers will offer for your car.

Tip: Get multiple offers to avoid underpricing.

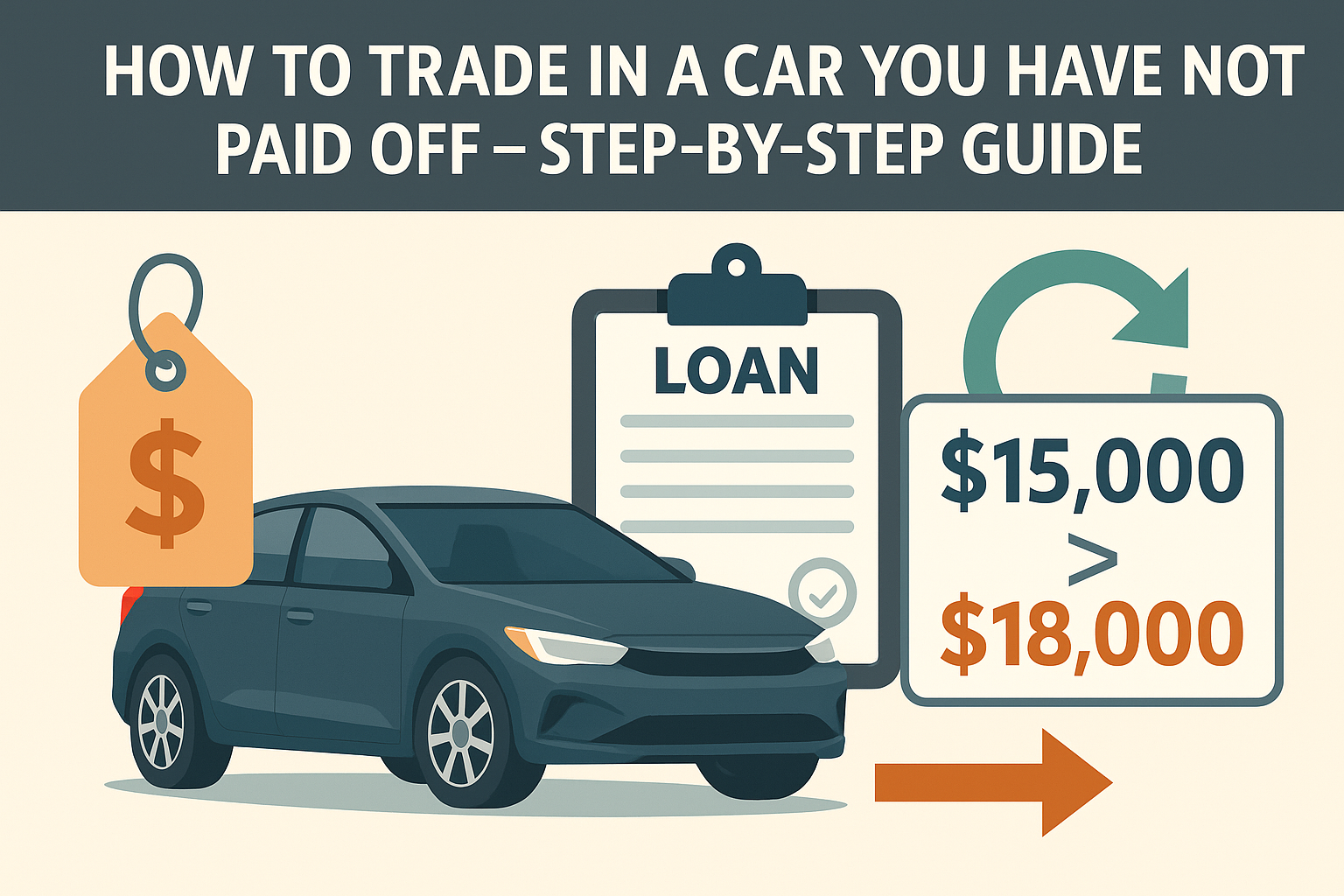

Step 3: Compare Trade-In Value vs. Payoff Amount

Now compare the numbers:

Positive Equity: If your trade-in value is higher than your payoff, you’re in good shape. The extra equity can go toward your next down payment.

Negative Equity: If your trade-in value is lower than your payoff, you have “upside-down” or negative equity. You’ll need to pay the difference or roll it into your next loan.

Example:

Car loan payoff: $18,000

Trade-in value: $15,000

Negative equity: $3,000

Step 4: Decide How to Handle Negative Equity (if any)

If you have negative equity, here are your options:

Pay the difference in cash at the dealership

Best choice to avoid increasing debt

Roll the difference into your next loan

Increases monthly payments and interest

Only do this if you’re buying a much more affordable car

Delay the trade-in

Continue making payments until you’re break-even or positive

Sell the car privately

May get a better price than trading in at a dealership

Could eliminate or reduce the negative balance

Step 5: Get Pre-Approved for Your Next Loan

If you’re trading in your car at a dealership, they’ll often handle the financing for your next vehicle—but it’s smart to get pre-approved from a bank, credit union, or online lender first.

Why?

You’ll know what APR you qualify for

You can negotiate from a position of strength

You’ll avoid surprise terms in the finance office

Step 6: Visit Dealerships with Your Payoff and Trade-In Info

Now you’re ready to shop. When visiting dealerships:

Bring your payoff amount letter

Share your title/lienholder info

Show any written trade-in quotes you’ve received

Ask for the “out-the-door” price of your next car (not just monthly payment)

Step 7: Review the Offer and Final Loan Structure

The dealer will calculate:

Your trade-in value

Your loan payoff

Whether equity or negative balance applies

Final monthly payments based on the next vehicle

Review carefully:

Confirm negative equity wasn’t padded with high fees

Don’t focus only on monthly payments—check loan term and total interest

Ask for a copy of all paperwork before signing

Step 8: Finalize the Trade and Vehicle Delivery

Once you agree to terms, the dealership will:

Pay off your current lender directly

Apply any positive equity to your new loan or down payment

Handle title transfer and registration

Finalize paperwork for your next vehicle

Your lender may take a few weeks to process the payoff, and you’ll receive confirmation when your old loan is closed.

Bonus Tip: Consider Selling Privately First

Selling your financed car to a private buyer may give you more money than trading it in. Here’s how:

Get the payoff quote

Find a buyer willing to pay close to retail value

Coordinate the payoff directly with the buyer and your lender

Use a secure payment method and provide the title once it’s released

Pros:

Maximize sale price

Possibly eliminate negative equity

Cons:

More effort and paperwork

Must handle transaction securely

Frequently Asked Questions

Can I trade in a car with a loan balance higher than its value?

Yes, but you’ll need to pay the difference or roll it into your new loan.

Does trading in a financed car hurt my credit?

No, as long as you continue making payments until the loan is paid off. Trading in can actually help if it reduces your debt load.

Can I trade in a leased car?

Yes, but it’s different—check the lease buyout price and compare it to the trade-in offer. You may owe early termination fees.

Final Thoughts: Trade Smarter, Not Faster

Trading in a car you haven’t paid off is totally doable—you just need to approach it with a clear understanding of your numbers. Know your payoff, get multiple trade-in quotes, and make sure the dealership’s offer works in your favor. The more prepared you are, the better the deal you’ll drive away with.